A SPAC-tacular Explosion

Here’s What You Need To Know

The announcement of a new industry group is a frequent occurrence in Washington, particularly as emerging sectors or practices gain attention –fairly or not – inside the Beltway. With such scrutiny, growing industries beef up their presence in Washington because in the world of Washington physics, political and reputational risks expand alongside newfound prominence and the disruption of the existing order. That’s why it was no surprise to see reports last month of a new group forming to represent the interests of special purpose acquisition companies, also known as SPACs.

Often, such coalitions arrive too late, after lawmakers, regulators, the press, and the public have formed views and demanded action. Smart public affairs professionals, however, get industry interests aligned before the onslaught, rallying the right mix of strategies to advance their business and policy objectives and avoid political and reputational pitfalls. For SPACs, there is no better time than now to get organized. Here’s what you need to know to understand why.

SPAC’s Lower Regulatory Burden Has Helped Spur Increased Popularity

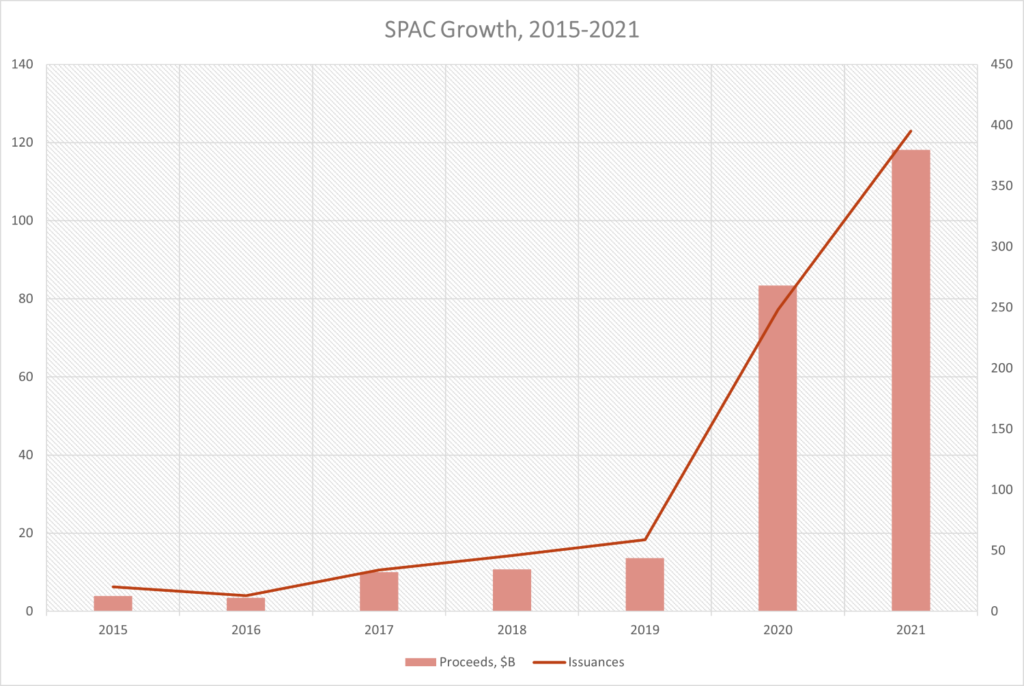

As IPOs Have Waned, SPACs Have Gained: A special purpose acquisition company (SPAC), according to CNBC, is “set up by investors with the sole purpose of raising money through an IPO to eventually acquire another company.” As we noted last year, such ‘blank check companies’ have become an attractive funding source for businesses due “in large part to the imposition of more stringent regulatory frameworks” that made traditional IPOs “increasingly unattractive to entrepreneurs and investors alike.” To avoid the regulatory complexity and intense public scrutiny of IPOs, greater numbers of startups have turned to SPACs as accessible financing tools to grow their organizations. In fact, 2020 saw an unprecedented number of SPAC IPO transactions, with last year’s offerings accounting for one-third of SPACs established over the past decade, and 2021 is already ahead of 2020.

Subscribe to Receive Insights

"*" indicates required fields

But Fewer Rules and Increased Popularity Come With More Risk

More Money, More Pressures: While such entities been around for some time, they have rapidly ascended in popularity over the past two years – vaulting from just 20 issuances in 2015 to nearly 400 already this year, with 50% more capital raised in the average deal. Such growth means more SPACs wooing the same investors to chase the same deals – and because of the former, doing so faster. This pace of activity means increased scrutiny and even pushback from investors and lawmakers alike, leaving SPACs with as many public affairs challenges as opportunities.

A Blank Check That Could Bounce: While SPACs have many attributes that make them attractive offerings for prospective investors, some government officials and financial experts warn of risks associated with investing in them. Chief among them is SPACs’ past performance. A Goldman Sachs index of 200 SPACs saw an average loss of 17 percent in 2021, compared to a 10 percent return in the S&P 500. Stephen Deane of the CFA Institute told Congress that each year since 2010, SPACs performed worse than the Russell 2000 by 10 percent or more. These results mean a SPAC investor must be exceptionally savvy and able to sustain significant losses, but Bank of America reports retail investors still account for 40 percent of SPAC trading on its platform, and some SPAC transactions are increasingly reliant on their appeal to such investors. Moreover, because a SPAC does not disclose outright what company it intends to acquire, investors have no idea in which business they are ultimately investing. With limited options in “hot” sectors like electric vehicles and fintech, investors are potentially financing SPACs that acquire less than desirable organizations with real problems or little market appeal.

Time Crunch Mean Less Due Diligence: According to Bloomberg News, “half the blank-check companies that filed for U.S. listings since the start of June are giving themselves an initial period of 18 months of less to find an acquisition target,” and many recently formed SPACs are pledging to merge within 12 months. Previously, more than 80 percent had set their duration at a standard 24 months, but with an explosion of SPACs chasing the same pool of investors, some are promising to move quicker to attract capital. To move with such speed, due diligence is necessarily performed at a narrower scope and faster pace than during an IPO, leaving SPACs vulnerable to potential restatements, incorrectly valued businesses, or even lawsuits and fraud. In addition, since a SPAC is already public, the target company won’t have an underwriter, which in a traditional IPO would ensure all regulatory requirements are met.

Related Posts:

That Means SPAC’s Influence-building Must Speed Ahead of Their Challenges

Wild West No More: SPACs’ growing popularity means more scrutiny – and enforcement – from regulators. In mid-July, the Securities Exchange Commission (SEC) charged a company and the SPAC that took it public with defrauding investors, explaining its case illustrated “risks inherent to SPAC transactions, as those who stand to earn significant profits from a SPAC merger may conduct inadequate due diligence and mislead investors.” The SEC is also investigating complaints against a variety of other SPAC-backed companies, including Lordstown Motors, Nikola Corp., Clover Health Investments, Akazoo SA, and Ability Inc. Since their ability to avoid costly and time-consuming red tape is one of SPACs’ most appealing qualities, SPAC managers who attract increased regulatory interest could lose investors or cause headaches for others in the industry. It also means businesses seeking to be acquired will still need to understand how well they can withstand the scrutiny that comes with being a publicly-traded corporation.

“Worth Of Our Attention” On Capitol Hill: Federal lawmakers across the political spectrum are taking notice of the SPAC boom as well. In April 2021, Sen. John Kennedy (R-La.) introduced legislation to “increase transparency surrounding blank-check companies,” averring in a statement that “[celebrities] are often the public face of companies selling shares to hardworking Americans” who do not understand the investments they’re making. His fellow Senator Tom Tillis (R-NC) noted, “These are just new creations that we don’t fully understand … We should probably look at whether or not Congress should play a role in regulation.” In May, the House Financial Services Committee, chaired by Rep. Maxine Waters (D-Calif.), held a hearing on that very question, with witnesses “broadly agreed on the need for reforms to liability protections for forward-looking statements by special purpose acquisition companies, a key regulatory disparity highlighted by the recent SPAC surge.” In advance of the hearing, Rep. Brad Sherman (D-Calif.) proposed legislation that would do just that, arguing, “I would be flabbergasted if we looked at this area and saw that there were no problems at all worthy of our attention.”

It’s Not Just The Government Taking Notice: For the moment, SPACs might be enjoying relatively free movement and robust growth, but as every sector can surely attest, government rarely passes up an opportunity to regulate or otherwise involve itself in commercial activity that captures headlines. And like every opportunity for government to step in, there will be advocates pressing for action and shaping the form that action takes. As Healthy Markets’ Tyler Gellasch warned, “When SPACs … had valuations all heading to the moon, there wasn’t a lot of tire-kicking on the real risks to investors, but now that some of the risks are turning into losses, we expect a lot more congressional and regulatory focus.” That means SPAC supporters must step smartly and carefully through the Washington landscape that in the past decade has grown ever more skeptical of financial markets’ ability and willingness to self-regulate. That means understanding their vulnerabilities, identifying allies and detractors, and ensuring that as political pressures mount, so, too, do their efforts to educate policymakers before it is too late.