The Public Market Disconnect

Here’s What You Need To Know

In a late April letter, Citigroup’s global head of credit strategy marveled that “the gap between markets and economic data has never been larger.” Even as stocks are on-pace to exceed previous peaks, 7.5 million small businesses face the prospect of permanent closure and 41 million Americans are out of work. Indeed, the true picture of job losses may be far worse than the unemployment number indicates. Yet major stock market indices are well on their way to regaining pre-pandemic and historic highs. As The Washington Post noted this week, “[M]any market players … remain stumped by the speed of the rebound in stocks amid the wider economic wreckage wrought by the pandemic shutdowns.”

This disconnect illuminates the reality that the stock market no longer serves as a reliable indicator of the strength of the American economy. In recent years, radical transformations in how investments are made have increased the unpredictability of the market, while long-term investors – who often hold funds tied to market indexes or targeting retirement dates – are less reactive to the highs and lows of such volatility. Meanwhile, the introduction of greater regulatory burdens has discouraged companies from going public, with many instead relying upon cash injections from private equity and venture capital to meet their funding needs until well after their companies mature.

This new reality now pervades the investment industry, and it puts private equity and venture capital firms in an important position for the economic recovery. While they long have been the subject of animus and scrutiny, particularly from their unfailing detractors in politics and the media, they now hold a far different place in the economic landscape than many policymakers or the market participants themselves realize. Although these firms might operate in private markets, they now serve a vital public purpose, which means policymakers must see them as the vital economic actors they have become, while the firms must ensure they act as good corporate citizens who can withstand this heightened public scrutiny.

Subscribe to Receive Insights

"*" indicates required fields

To adapt this new reality and what it means for your interests, here’s what you need to know:

The Stock Market Used To Tell Us How the Economy Is Doing. Not Anymore.

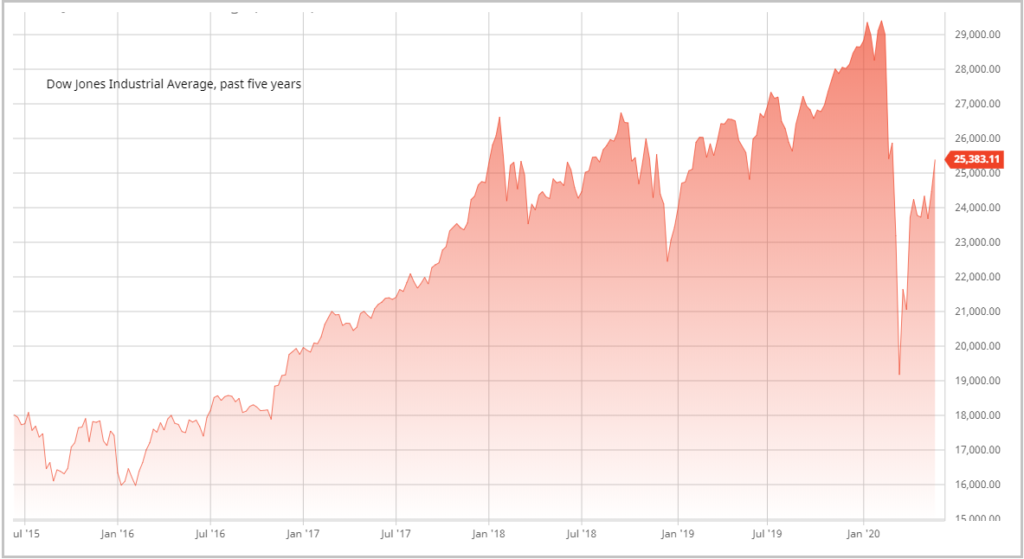

There’s No Business Like Big Tech Business: On March 20, 2020, the U.S. stock market made its deepest dive since the Great Depression, erasing years’ worth of gains and plummeting to fewer than 19,200 points. Today, the Dow Jones Industrial Average (DJIA) is already nearly 6,000 points above its position when President Trump took office on January 20, 2017 and has recovered a great deal of its coronavirus losses. This gain is due in large part to tech giants like Facebook, Amazon, Apple, Netflix, and Google – known colloquially as the FAANG stocks – soaring. Since the March 20th valley, Facebook has grown 57 percent, Amazon is up 31 percent, Apple has risen by 39 percent, Netflix is up 24 percent, and Google has grown 28 percent. Even in the midst of a global pandemic, the stock value of all FAANG companies remains at their highest-ever. The Economist chalks it up to investors “despairing[ly] reaching for the handful of businesses judged to be all-weather survivors.” In this case, those all-weather survivors make up one-fifth of the value of the entire S&P 500 Index – and they have given the rest of the stock market reason to breathe a sigh of relief and start investing again.

Balance of Trade: Over the past several years, significant changes in how and when Americans invest have transformed the economy. Thanks to the creation of 401(k) plans in 1978, average Americans now ride the stock market long-term, directing much or all of their retirement savings to the stock market. In 1990, 401(k)s controlled $384 billion in assets. In just thirty years, that amount has risen to $4.8 trillion, a more than 1200 percent increase in value. Much of these investments are dedicated to index funds or target date funds rather than individual stocks, leaving these funds with a large supply of incoming dollars that must find an investment home, regardless of then-current market conditions. Meanwhile, experts say that high-frequency trading has changed the algorithm of investing, making the markets more volatile and creating exceptionally high peaks– and in the case of coronavirus, exceptionally low valleys – in the stock market. This shift is due to expanded access to technology that has replaced expert traders with computerized models, which some analysts argue can ignore legitimate analysis and common sense.

Related Posts:

The American Economy Is Now Built in Private Markets

The “Listing Gap”: In recent years, the American marketplace has seen fewer Initial Public Offerings (IPOs). In fact, only 3 percent of venture-backed companies went public in the last decade. As Business Insider’s Bob Bryan noted, a 2015 study “found that the US had developed a ‘listing gap’ between the number of firms that should be listed based on the country’s economic development and the shrinking number that are. … At the peak in 1996, there were 8,025 publicly listed US companies; as of 2012 that number was down to 4,102.” This drop came even though historic U.S. economic data suggested “9,538 should have been listed,” leaving “a ‘gap’ of 5,436 listings.” This massive split is due in large part to the imposition of more stringent regulatory frameworks like Sarbanes-Oxley Act in 2002 and Dodd-Frank in 2010, both of which made going public increasingly unattractive to entrepreneurs and investors alike.

The New Business of Big Business: This listing gap has shifted the balance of financial power toward venture capital and private equity, which has allowed start-ups to maintain more autonomy, and investors to avoid added disclosures, all while creating wealth and growing companies without tapping public markets. Indeed, as entrepreneurial financial expert Greg Crabtree explained in a Growth Institute blog post: “Entrepreneurs used to need the public markets for liquidity. That is not the case anymore. There is so much money in the market looking for a place to go that liquidity is easily solved. In every deal we have seen in the last couple of years, the private equity firms have been offering as good of a deal as any public company has in a purchase or investment scenario.”

Private Equity’s Role: These days, companies are often delaying going public as long as they can, thanks to greater funding availability made possible by private equity. There is perhaps no greater example of the powerful role of private equity in transforming this dynamic than with Uber. Bain & Company calls the rideshare company the “poster child” for private equity, as it rode $21 billion in venture capital to a private valuation of approximately $72 billion. Although it had been in business since 2009, Uber Technologies, Inc. took a decade to go public and only did so to access enough capital to pay out investors and shareholders. Bain & Company argues Uber’s examples shows “the advantages of going public no longer outweigh the considerable disadvantages,” as private equity frees up companies to borrow at historically low rates while avoiding the “myriad costs and hassles of going public.”

Even Public Markets Are Focused on Private Enterprise: Further demonstrating this shifting dynamic is the keen interest in Special Purpose Acquisition Companies (SPACs), which are often and sometimes derisively called “blank-check” companies, which can raise money through an IPO for the sole purpose of buying other companies. According to Pitchbook, SPACs have “accounted for 38 percent of U.S. IPO filing and raised $6.5 billion as of May 20 – more than the total capital raised by institutionally-based IPOs during the period.” Experts attribute some of this interest to the coronavirus pandemic, because “as private companies’ valuations fall and they look for liquidity, SPACs could fill a void left by traditional IPOs,” but like many pandemic-connected observations, the trend began beforehand and has been accelerated by the virus.

As Private Equity’s Role Grows, so Will Public Scrutiny

Leading the Way: As millions of American businesses face coronavirus lockdown-induced closures, private equity will take center stage to reinvigorate the country’s emblematic entrepreneurship. Private equity will continue to give entrepreneurs the unique space to be creative and to take risks in ways that more traditional investing models do not. As Bloomberg News quipped late last year, “everything is private equity now.” With growing numbers of American businesses from pet shops to real estate agencies already relying upon private equity firms to fund their growth, PE will help reshape the new American economy.

Changing the Narrative: With a crucial role to play in the recovery, private equity must face its reputational challenges head-on. For decades, leftwing policymakers have vilified the private equity industry as reckless gamblers, relying upon the investments of ordinary people to place risky bets and saddle enterprises with unsustainable debt. The media have echoed these claims, with some insisting private equity should be pushed out in the recovery. As private equity’s role in the economy continues to take center stage, that scrutiny will grow with it – but it also means policymakers will need to reach an uneasy peace with private equity. Whether policymakers like it or not, cutting PE-backed firms out of pandemic relief programs and other such measures will not be tenable if the country is to regain its economic momentum.

Still, private equity firms will also need to appreciate their new public purpose. That must begin with refuting its persistent negative image. As The Economist explained in a recent analysis, the PE industry is vital not only for its investors but also for the overall recovery of the global economy. This requires them to engage in efforts long understood by publicly traded companies to bolster public trust. Doing so will require understanding and anticipating the accompanying political and reputational risks and getting ahead of them. That’s where Delve offers them – and anyone looking for competitive intelligence support – a real advantage.